Table of Contents

ToggleMoney Market Calculator: Project Your Savings Growth

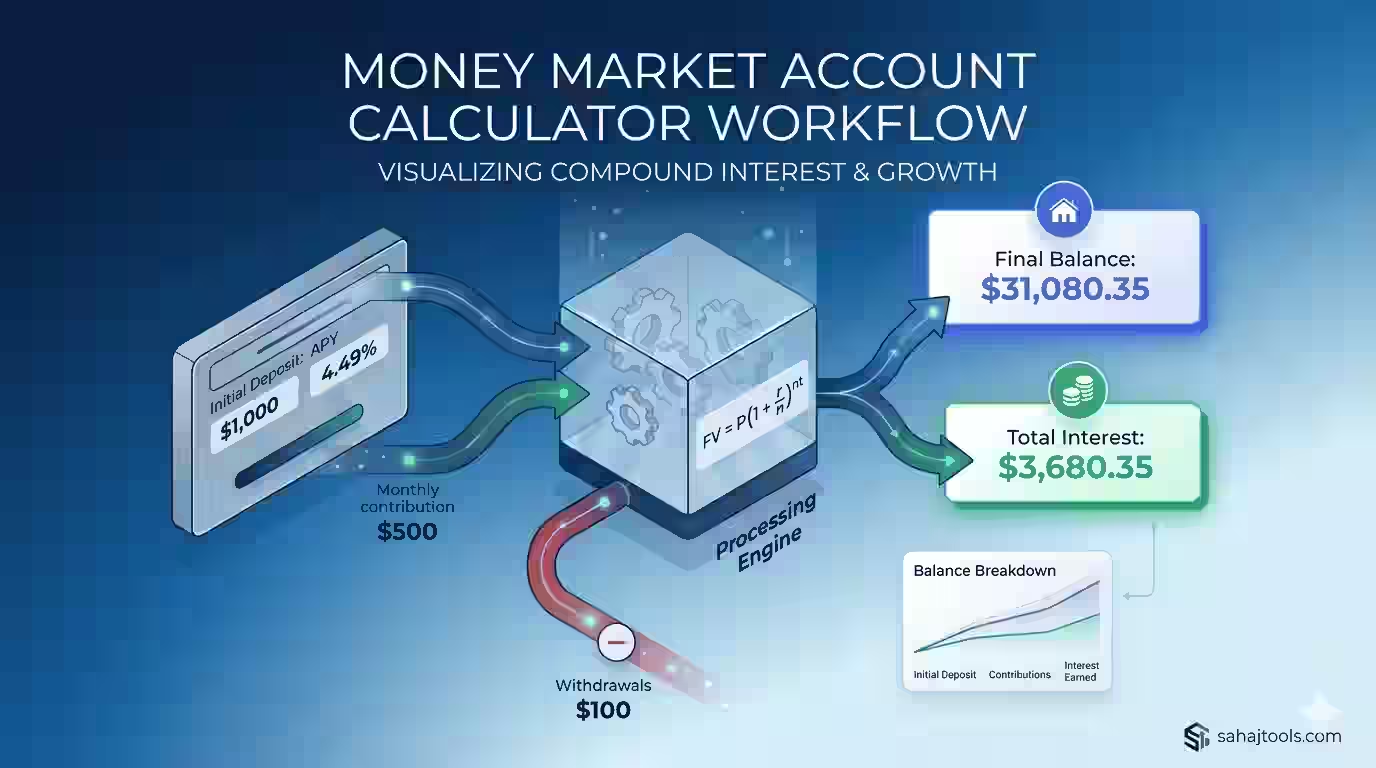

An online Money Market Calculator helps you estimate how much your savings will grow over time by factoring in dividend yields, compounding frequencies, and recurring contributions. By modeling these financial variables, this money market account calculator lets you determine exactly how your principal scales under modern banking environments.

Money Market Account Calculator

Accurate compound interest projections with real banking formulas

APY already accounts for compounding — enter the rate shown by your bank.

$

%

yrs

mos

$

$

Withdrawals are applied after interest each month.Final Balance—

Total Interest—

Total Contributions—

Effective APY—

Balance Breakdown

Initial Deposit

—

Contributions

—

Interest Earned

—

Year-by-Year Breakdown

| Year | Balance | Interest | Contributions | Withdrawals |

|---|

Calculations use compound interest: FV = P(1 + r/n)nt + annuity formula. Estimates only.

Reset Calculator?

This will clear all inputs and results.

related finance & business calculators

What Is a Money Market Account?

A Money Market Account (MMA) is a hybrid financial instrument offered by banks and credit unions that combines the features of a traditional savings account with basic transactional capabilities, such as standard check-writing privileges or debit card access. When using a money market savings account calculator, your calculations are structured around two baseline components: your initial deposit (the principal amount) and your ongoing contributions.

Money market accounts traditionally yield higher interest returns than basic savings vehicles because financial institutions pool these deposits to invest in short-term, low-risk debt securities, such as U.S. Treasury bills and commercial paper. The yield you receive, typically designated as money market account interest or the money market account APY, fluctuates based on broader macroeconomic targets established by the Federal Reserve Board. Understanding your projected performance helps you select institutional terms that align with your risk tolerances.

How It's Calculated: The Math Behind Compound Interest

To accurately project savings growth, a comprehensive money market interest calculator acts as a unified compound interest calculator. The ultimate balance depends entirely on whether your chosen institution prices its returns using a simple nominal interest rate or an annual percentage yield (APY), alongside the specific frequency of its calculation intervals.

What is the formula for money market interest?

The math driving our tool utilizes the classic compound interest formula combined with an ordinary annuity equation to handle periodic additions. The mathematical representation is:

Future Value = Principal * (1 + (Rate / Frequency))^(Frequency * Years) + Contribution * (((1 + (Rate / Frequency))^(Frequency * Years) – 1) / (Rate / Frequency))

Where:

- FV = Future Value (the final balance of your money market portfolio)

- P = Principal amount (your initial deposit)

- r = Annual nominal interest rate (expressed as a decimal)

- n = Compounding frequency per year (e.g., 12 for monthly compounding, 365 for daily compounding)

- t = Total investment term in years

- PMT = Periodic contribution amount (monthly deposit)

What is the difference between APY and interest rate?

The nominal interest rate reflects the base percentage paid by the bank before accounting for intra-year interest generation. Conversely, the Annual Percentage Yield (APY) represents the true annualized rate of return, incorporating the compounding effects within a single 12-month sequence. If a bank quotes a nominal interest rate, the actual earnings estimate rises alongside compounding intervals. If they quote an APY directly, the mathematical formula adjusts because compounding is already embedded within that statutory figure.

How often does interest compound in a money market account?

Most contemporary domestic banking systems run an automated tracking ledger that utilizes either monthly compounding or daily compounding.

If your final balance falls short of your financial milestones, you can easily tweak your monthly contributions or find an account with higher money market account rates to accelerate your savings engine.

What happens when compounding is monthly versus daily?

When compounding occurs daily, a micro-fractional percentage of interest is computed every single day based on your current balance and added to your capital. This newly generated sum immediately begins earning its own interest the very next day. While daily calculation yields a slightly higher nominal return over decades than monthly adjustment, the difference on modest balances is typically razor-thin. This relationship is precisely mapped inside the application software.

How to calculate money market growth manually?

If you choose to track your growth manually without an interactive digital tool, you can break the equation down month-by-month:

- Divide your annual nominal rate by 12 to find your monthly yield.

- Multiply your starting balance by this monthly value to calculate that month’s interest payment.

- Add the interest payment and any monthly contribution to your balance.

- Repeat the step sequence sequentially for each consecutive calendar month of your target timeline.

Step-by-Step Guide to Projections

To execute standard calculations, configure the interactive web system layout using the parameters shown in the user interface file Money-Market-Account-Calculator-Grow-Your-Savings-Fast-06-23-2026_08_13_PM.png. This specialized money market rate calculator runs entirely in-browser via secure client-side computing scripts to ensure user data remains completely private.

Follow these specific operating guidelines to build your forecast:

- Select Your Interest Rate Type: Toggle between the APY and APR input options located at the crown of the console dashboard. Selecting APY automatically handles compounding adjustments natively.

- Define Your Initial Deposit: Enter your baseline starting capital into the Initial Deposit field. This serves as the original structural core of your savings engine.

- Input Your Annual Rate: Provide your current bank rate into the APY Interest Rate percentage box.

- Set Your Compounding Frequency: Choose your appropriate operational schedule from the drop-down menu (e.g., Monthly or Daily execution paths).

- Establish Your Investment Duration: Define your planned timeline across the synchronized Year (yrs) and Month (mos) parameters. This sets the total investment term.

- Incorporate Optional Cash Flows: Utilize the Monthly Contribution field to model recurring additions, or use the Monthly Withdrawal parameters to evaluate regular cash outflows.

- Generate Results: Click the primary blue Calculate action trigger to render your final future value projections instantly.

Worked Examples: Future Value Scenarios

To demonstrate how these variables interact under true market scenarios, review the following two cash flow pathways modeled by an investment growth calculator.

Scenario A: The Long-Term Wealth Accumulator

Suppose an investor starts with a strong initial footprint and commits to regular, steady growth over an extended horizon.

- Initial Deposit (P): $10,000

- Stated APY (r): 4.50%

- Compounding Cadence (n): Monthly (12x/year)

- Total Duration (t): 5 Years

- Monthly Contribution (PMT): $500

Running these parameters through the mathematical engine delivers a clear earnings estimate showing how continuous contributions reshape terminal asset value.

- Total Contributions: $30,000 over 60 months

- Total Interest Earnings: $5,249.12

- Final Balance: $45,249.12

Scenario B: The Lump-Sum Baseline Strategy

This scenario highlights an investor who deploys a large sum upfront without making subsequent recurring additions.

- Initial Deposit (P): $25,000

- Stated APY (r): 5.00%

- Compounding Cadence (n): Daily (365x/year)

- Total Duration (t): 3 Years

- Monthly Contribution (PMT): $0

Without regular additions, the performance relies entirely on the initial principal and the daily compounding mechanism.

- Total Contributions: $0

- Total Interest Earnings: $4,046.11

- Final Balance: $29,046.11

How much will a money market account earn over time?

As demonstrated above, earnings depend heavily on time and rate stability. Over a standard 10-year period, a $10,000 deposit at a steady 4.00% APY without extra contributions yields $4,802.44 in total interest. If you extend that timeline to 20 years, the interest earned grows to $11,911.23, demonstrating the exponential nature of compound growth.

How do monthly deposits change the final balance?

Regular contributions fundamentally accelerate your portfolio’s growth curve. Adding just $100 per month to an initial $5,000 account balance over 5 years at 4.50% APY shifts your final balance from $6,230.91 to $12,987.89. This simple habit more than doubles your final savings pool.

What initial deposit is needed to reach a savings goal?

If you intend to accumulate a fixed target of $20,000 within a 4-year timeframe at a 4.00% APY without adding supplemental funding, you can reverse-engineer the math. Using a final balance calculator framework shows you would need a starting deposit of $17,096.08 to hit that objective purely through passive growth.

Scenario & Rate Comparison Table

To evaluate your structural options across different product lines, utilize this comparison table mapped via an APY calculator and savings growth calculator:

Financial Institution / Product Tier | Stated APY (%) | Initial Principal ($) | Monthly Contribution ($) | Horizon (Years) | Estimated Final Balance ($) |

High-Yield MMA (Tier 1) | 5.00% | $5,000 | $250 | 5 | $22,465.34 |

Mid-Market Bank MMA | 4.00% | $5,000 | $250 | 5 | $21,833.10 |

Traditional Savings Account | 0.50% | $5,000 | $250 | 5 | $20,195.42 |

How to compare different money market rates?

When shopping for competitive returns, look beyond the headline APY. Check the institution’s minimum balance rules to ensure you won’t trigger monthly maintenance fees, which can quickly wipe out your interest earnings. This step is critical before moving your money.

Risk Factors, Trade-offs, and Market Realities

While money market accounts offer excellent capital security, they carry structural constraints that savers must carefully consider:

- Inflationary Risk: Money market yields generally track federal funds rates. During inflationary periods, your real rate of return (nominal yield minus inflation) can turn negative, slowly eroding your purchasing power over time.

- Variable Rate Fluctuations: Unlike a Fixed-Rate Certificate of Deposit (CD), an MMA carries a variable interest rate. Banks can adjust their paid APY at any time in response to shifting market conditions.

- Yield Caps and Balance Tiers: Many financial institutions use tiered pricing structures. You might earn a premium rate on your first $25,000, while balances above that threshold drop to a much lower tier.

Common Mistakes to Avoid

- Overlooking Minimum Balance Requirements: Many institutions require a high minimum balance to secure their top-tier APY. Falling below this threshold can trigger monthly maintenance fees that outpace your interest earnings.

- Treating an MMA Like a Standard Checking Account: Although MMAs provide debit or check-writing access, excess transactions can trigger institutional fees or cause the bank to reclassify your account.

- Neglecting the Power of a Monthly Savings Calculator Strategy: Relying solely on your initial deposit misses the wealth-building potential of automated monthly contributions. Consistently adding small amounts optimizes your long-term compound growth.

related finance & banking calculators

- Money Market Calculator: Plan your investments alongside spousal support payments. This tool helps you estimate returns on savings or investments, ensuring you can meet financial obligations while growing your wealth.

Frequently Asked Questions

No, provided your account is held with an FDIC-insured commercial bank or an NCUA-insured credit union. Your principal is legally protected up to $250,000 per depositor, making these accounts exceptionally secure.

Yes. The interest earned in an MMA is treated as ordinary taxable income by the IRS. Your institution will issue a Form 1099-INT each year detailing your earnings for tax reporting.

Neither is universally better. HYSAs often feature lower initial deposit thresholds, while MMAs provide more flexible access to your funds through check-writing and debit card options.

Because MMAs feature variable rates, institutions can adjust their yields at any time. These shifts typically follow changes in the federal funds rate set by the Federal Reserve.

reference list

- Federal Deposit Insurance Corporation (FDIC) – Learn about deposit insurance limits and bank safety.

- National Credit Union Administration (NCUA) – Check savings protections for credit union money market accounts.

- Federal Reserve Economic Data (FRED) – Review historic and current national money market rate trends.

- Consumer Financial Protection Bureau (CFPB) – Access consumer guides on choosing deposit accounts wisely.

Disclaimer

All calculations and projections provided by this tool are for educational and estimation purposes only. Actual interest rates, account fees, compounding methods, and qualification terms vary by financial institution and depend on your account balance. This application does not provide formal financial, tax, or investment advice. Consult a qualified financial advisor or check directly with an FDIC-insured institution before making major capital allocations.

A money market account serves as an excellent financial tool for growing your liquid savings without sacrificing accessibility. Utilizing a Money Market Account Calculator allows you to accurately map your future wealth, compare competing bank rates, and see the tangible impact of regular monthly contributions. Take control of your financial goals today by adjusting the variables in our calculator to build your ideal savings plan.

Ready to see your savings grow? Enter your numbers into the Money Market Account Calculator above and start planning today!

Last Update: June 2026