Table of Contents

ToggleUK Rent Affordability Calculator — Know Your Budget

A UK rent affordability calculator tells you how much rent you can afford based on your gross income, monthly expenses, and the letting-agent 30× rule (annual salary ÷ 30 = maximum monthly rent). For a £35,000 salary, the maximum affordable rent is £1,167/month. Use the calculator below to find your personal Safe, Stretch, and Over Limit thresholds instantly.

UK Rent Affordability Calculator

Based on verified UK letting agent standards & the 30× income rule

01Your Income

£

£

02Property Rent (optional — check a specific property)

£

03Monthly Expenses (your take-home / net income budget)

£

£

£

£

£

£

04UK Region

Your Affordability Report

Max Affordable Rent—per month (30× rule)

Conservative Range—25% of gross income

Stretch Limit—35–40% of gross income

Guarantor Needed If Over—Guarantor requires 36× income

Income-to-Rent Ratio

Safe

25%30%StretchOver limit

25%30%StretchOver limit

0%

Safe ≤25%Standard 26–30%Stretch 31–40%High Risk >40%

Monthly Budget Breakdown

UK Letting Agent Check (30× Rule)

| Check | Required | Your Figure | Result |

|---|

Recommendations

Calculations use the standard UK 30× letting-agent rule (annual gross income ÷ 30 = max monthly rent), the 30% gross income benchmark, and the 36× guarantor requirement, as used by OpenRent, Rightmove partner agents, and most UK referencing providers. Regional adjustments reflect documented market conditions. This calculator does not constitute financial advice.

Reset Calculator?

This will clear all your inputs and results.

related finance & banking calculators

What Is a Rent Affordability Calculator?

A rent affordability calculator is a free online tool that estimates the maximum monthly rent you can comfortably pay based on your income, existing expenses, and standard landlord referencing rules. It combines gross income analysis, net take-home modelling, and UK-specific letting agent benchmarks to give you a complete picture of your housing budget before you ever speak to an agent.

Beyond simple lease payment affordability, a good UK rental affordability calculator also flags whether a specific property will pass the landlord’s reference check, calculates the guarantor income required if it does not, and breaks your net income into rent, expenses, and savings — so you can see whether a property is genuinely affordable day-to-day, not just on paper.

This tool is built for prospective renters, budget-conscious households, and lease applicants across England, Scotland, and Wales who want to approach a tenancy application with confidence.

How Rent Affordability Is Calculated

The calculator applies four distinct benchmarks that UK letting agents and money-advice services use. Understanding each one helps you interpret your results.

The 30× Annual Income Rule (Landlord Reference Check)

Annual gross income ÷ 30 = maximum monthly rent.

This is the primary check used by Rightmove partner agents, OpenRent, and most independent referencing providers. It is based on gross income — your salary before tax and National Insurance — not your take-home pay. On a £35,000 salary, the threshold is £1,167/month. A property at £1,200/month would fail this check because £1,200 × 30 = £36,000, which exceeds the tenant’s £35,000 income.

The 30% Gross Income Benchmark

Monthly rent ÷ Gross monthly income × 100 = rent-to-income ratio. Result should be ≤30%.

This is mathematically identical to the 30× rule — just expressed as a percentage of monthly rather than annual income. It is the standard guideline promoted by MoneyHelper and most UK housing charities.

The 25% Conservative Range

Allocating no more than 25% of gross monthly income to rent leaves a meaningful savings buffer and reduces rent burden. On a £35,000 salary, this gives a conservative ceiling of £729/month.

The 36× Guarantor Rule

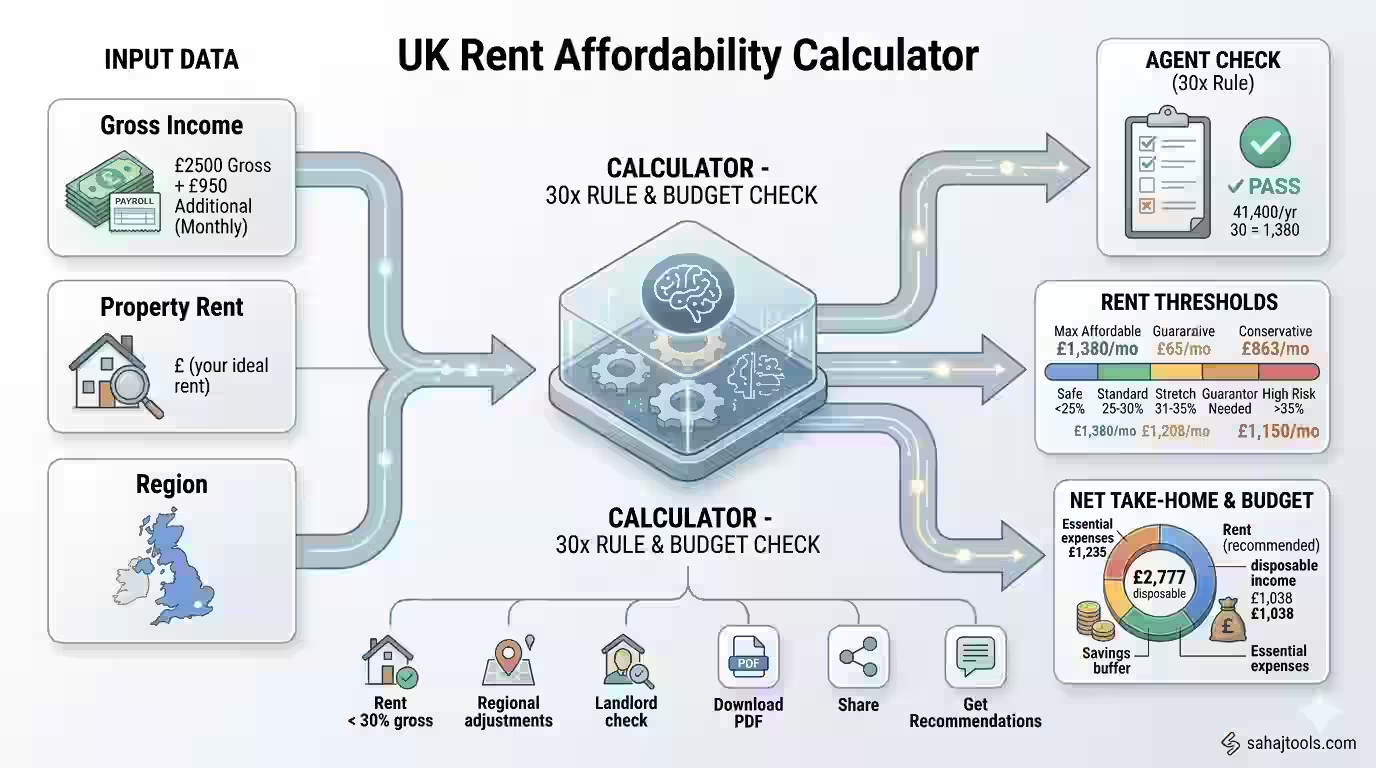

A renter in South East England earns £2,500/month gross plus £950/month additional income (e.g., freelance work), giving a combined gross of £3,450/month or £41,400/year.

What About the 28/36 Rule and 50/30/20 Rule?

The 28/36 rule originates in the US mortgage market and is not applied by UK letting agents — do not use it when assessing a UK tenancy application. The 50/30/20 budgeting rule (50% needs, 30% wants, 20% savings) is a useful complementary personal finance framework, but it is not a landlord referencing threshold.

Rent-to-Income Thresholds at a Glance

Band | Rent-to-Income Ratio | What It Means |

Safe | ≤ 25% | Low rent burden; comfortable headroom for savings and unexpected costs |

Standard | 26–30% | Within the UK letting-agent threshold; passes most referencing checks |

Stretch | 31–40% | Feasible in high-demand areas; reduced saving capacity; may still pass with a guarantor |

Over Limit | > 40% | High rent burden; likely to fail standard referencing; guarantor strongly recommended |

Income-to-Rent Rule Summary

Rule / Benchmark | How It Works | When It Applies |

30× Annual Income Rule | Rent ≤ Gross Income ÷ 30 | Standard UK letting agent check — used by Rightmove partner agents, OpenRent, and most referencing providers |

30% Gross Income Benchmark | Monthly rent ≤ 30% of gross monthly income | General affordability guideline; widely referenced by money-advice services including MoneyHelper |

25% Conservative Range | Monthly rent ≤ 25% of gross monthly income | Comfortable buffer zone; recommended for renters with higher debt or variable income |

35–40% Stretch Limit | Monthly rent 35–40% of gross income | Acceptable in high-demand regions (e.g. Greater London, South East England, Brighton, Oxford) where supply is constrained |

36× Guarantor Rule | Guarantor’s income must be ≥ rent × 36 | Required when the tenant fails the 30× check; guarantor is jointly liable for the tenancy |

How to Use the UK Rent Affordability Calculator: Step-by-Step

The calculator is divided into four numbered sections. Work through them in order, then click Calculate Affordability.

- Section 01 — Your Income. Select Annual or Monthly using the toggle at the top. Enter your gross salary (before tax) in the Your Gross Income field. If you have a second income stream — a bonus, freelance work, or part-time earnings — add it in the Additional Income field. The tool uses gross figures for the landlord check and estimates your net take-home separately.

- Section 02 — Property Rent (optional). Enter the monthly rent of the specific property you are considering in the Monthly Rent to Check field. If you leave this blank, the calculator will still return your general maximum affordable rent and savings band, but the pass/fail landlord check will not appear.

- Section 03 — Monthly Expenses. Expand this section by clicking the Advanced link. Enter your recurring monthly outgoings across six fields: Debt Repayments (loans, credit cards, car finance), Food & Groceries, Transport, Bills & Utilities (gas, electricity, broadband, council tax), Childcare/Education, and Other Expenses. These figures do not affect the landlord reference check, but they do determine your real-world monthly housing budget and the savings buffer shown in the donut chart.

- Section 04 — UK Region. Select your region from the dropdown. Regional data adjusts the stretch-limit guidance, because renters in Greater London, South East England, and other high-demand areas are typically expected to stretch to 35–40% of gross income.

- Click Calculate Affordability. Your Affordability Report appears below the button. It shows Max Affordable Rent, Conservative Range, Stretch Limit, Guarantor Needed If Over threshold, the income-to-rent ratio bar, and the Monthly Budget Breakdown donut chart. If you entered a specific property rent in Step 2, you will also see a pass/fail result against the 30× rule and the 30% gross income benchmark.

- Download or Copy. Use the Download PDF button to save your Affordability Report, or Copy Summary to paste the key figures into a message. Use Reset to clear all fields.

Worked Example: South East England, £35,000 Salary

The following example matches the calculator output shown on this page. It illustrates how a renter with a £35,000 gross salary fares against a £1,200/month property in South East England.

Input / Output | Value |

Gross annual income | £35,000 |

Income mode | Annual |

Monthly rent to check | £1,200 |

Monthly expenses (total) | £0 entered |

UK region | South East England |

Max affordable rent (30× rule) | £1,167/mo |

Conservative range (25% gross) | £729/mo |

Stretch limit (35–40% gross) | £1,021/mo |

Guarantor needed if rent exceeds | £972/mo (36× rule) |

30× annual income rule | FAIL — need £36,000/yr for £1,200/mo |

Estimated net take-home | ≈ £2,393/mo |

Rent-to-income band | Over Limit (41.1% of gross) |

Interpretation: The tenant’s income fails the standard 30× check by £1,000/year. However, the estimated net take-home is £2,393/month, which leaves £1,193/month after rent — a meaningful real-world buffer despite the technical referencing shortfall. A guarantor earning at least £43,200/year would satisfy the 36× check and likely allow the tenancy to proceed.

Factors That Affect Your Affordable Rent

- Gross income level. The 30× rule is directly proportional to your gross salary. A £1,000 increase in annual income raises your maximum monthly rent by approximately £33.

- Recurring debt payments. Monthly debt repayments — personal loans, car finance, credit card minimums — increase your debt-to-income ratio and reduce disposable income without changing your gross salary. Agents typically view a high debt load as a secondary risk factor.

- Monthly housing costs beyond rent. Gas, electricity, broadband, and council tax are recurring monthly housing costs that are separate from rent but funded from the same take-home pay. Entering them in Section 03 ensures your budget breakdown reflects true housing affordability.

- Rent burden percentage. When rent exceeds 40% of gross income, you enter the Over Limit band. Most standard referencing agencies will flag this automatically, and many landlords will require a guarantor regardless of credit score.

- Employment type. PAYE employees can use gross salary directly. Self-employed renters should use the average net profit from their last 2–3 SA302 returns, as that is what agents will verify.

- UK region. The South East, Greater London, and other high-demand regions operate with an informal stretch allowance of 35–40% of gross income. Landlords in these areas regularly accept tenants whose rent-to-income ratio would fail in lower-cost regions.

- Additional income streams. Regular, evidenced additional income — a permanent part-time role, investment dividends, or rental income — can be included in the gross income figure. Irregular bonuses and commissions are handled differently by different agents.

UK Regional Letting Agent Standards

While the 30× annual income rule is applied nationally, regional variation exists in how strictly agents enforce the stretch limit.

- Greater London and South East England: Agents routinely accept rent-to-income ratios of 35–40% in Brighton, Oxford, Cambridge, and inner London boroughs, provided the tenant has a clean credit history. A guarantor is more frequently requested than in lower-cost regions.

- Scotland: The same 30× income rule is widely applied. Scotland’s Private Residential Tenancy (PRT) framework (governed by the Private Housing (Tenancies) (Scotland) Act 2016) provides stronger tenant protections but does not change referencing income thresholds.

- Wales: Standard UK letting-agent referencing rules apply. The Renting Homes (Wales) Act 2016 updated tenancy types but left the affordability-check methodology unchanged.

- Northern Ireland: Private Residential Tenancy rules differ from those in Great Britain. The same gross-income principles apply to affordability checks, but tenancy law is governed by the Private Tenancies Act (Northern Ireland) 2022.

Common Mistakes to Avoid

Mistake | Why It Matters |

Using net income for the 30× check | UK landlords assess gross (pre-tax) income. Entering your take-home pay will make your maximum appear lower than the agent’s actual threshold. |

Ignoring the 28/36 rule | The 28/36 rule originates in the US mortgage market and is not used by UK letting agents. Do not apply it to a UK tenancy application. |

Omitting recurring debt repayments | Credit card minimums, car finance, and student loan repayments reduce your disposable income and affect your real-world rent burden — enter them in the Debt Repayments field. |

Treating the stretch limit as the safe limit | Renting at 35–40% of gross income leaves little buffer for repairs, emergencies, or income dips. Aim for the 30% benchmark where possible. |

Self-employed: using gross turnover | Agents typically average your SA302 tax returns over 2–3 years. Your qualifying income is your net profit, not your gross revenue. |

Practical Tips for UK Renters

- Run the calculator before you view properties. Knowing your maximum affordable rent and referencing threshold before you schedule viewings prevents the disappointment of finding a property you cannot pass referencing for.

- Use the 50/30/20 rule as a complementary check. Once you know your net take-home from Section 03’s estimate, consider whether your total housing costs (rent plus utilities) fit within the 50% ‘needs’ bucket of the 50/30/20 framework. If housing alone exceeds 50% of net income, the property is likely too expensive regardless of whether it passes the 30× gross check.

- Factor in moving costs. Deposits (capped at five weeks’ rent under the Tenant Fees Act 2019), a holding deposit (one week’s rent), and removal costs are not reflected in the monthly budget but must come from savings.

- Arrange a guarantor in advance. If you are close to the 30× threshold, identify a guarantor before applying. Having the paperwork ready — guarantor’s payslips or SA302 returns — speeds the referencing process significantly.

Frequently Asked Questions

The standard UK guideline is that monthly rent should not exceed 30% of your gross monthly income, which corresponds to the letting-agent 30× rule (annual gross income ÷ 30 = maximum monthly rent). For example, on a £35,000 salary your maximum is approximately £1,167/mo. Use the calculator to see your full range, including conservative and stretch figures.

UK letting agents use two linked checks: (1) 30× Rule — Annual gross income ÷ 30 = maximum monthly rent; (2) 30% Gross Income Benchmark — Monthly rent ÷ Gross monthly income × 100 ≤ 30%. Both must pass. If your income falls short, a guarantor whose income meets the 36× rule (rent × 36 = minimum annual income) may satisfy referencing.

UK letting agents and referencing providers base their checks on gross income (before tax and National Insurance). However, your real-world affordability depends on your net take-home pay. This calculator shows both: the gross-based landlord check and your estimated net disposable income after tax.

Debt repayments — credit cards, car finance, personal loans — reduce your disposable income without changing your gross salary. This means you can pass a landlord's 30× check yet still be over-stretched in practice. Enter your monthly debt obligations in the Debt Repayments field to see an accurate monthly budget breakdown.

The 30% rent rule states that no more than 30% of your gross monthly income should go towards housing costs. It is used by UK letting agents as a referencing benchmark alongside the 30× annual income rule. Both rules produce identical thresholds; the 30× rule is simply the annual expression of the same 30% standard.

A ratio at or below 25% is considered Safe (comfortable headroom for savings). 26–30% is Standard and typically passes referencing. 31–40% is a Stretch zone — feasible in high-demand areas but leaves limited saving capacity. Above 40% is Over Limit and is likely to fail standard referencing without a guarantor.

Utilities — gas, electricity, broadband, council tax — are separate from rent but reduce the income available for housing. Enter your monthly bills and utilities in Section 03 of the calculator. The Monthly Budget Breakdown will then split your net take-home into rent, expenses, and savings buffer, giving you a complete picture of true housing costs.

Most UK landlords and letting agents use a referencing provider (such as Homelet, Let Alliance, or OpenRent's integrated checks) to verify: (1) the 30× annual income rule; (2) credit history and any county court judgements (CCJs); (3) employment status and payslips or SA302 returns for the self-employed. Passing the 30× threshold is usually the first filter applied.

Reverse the 30× formula: required annual gross income = monthly rent × 30. For a £1,200/mo property you need at least £36,000/yr gross. For a guarantor, the 36× rule applies: £1,200 × 36 = £43,200/yr minimum gross income.

Not necessarily, even if it passes the landlord check. The calculator's Monthly Budget Breakdown estimates your net take-home pay after tax and National Insurance, then deducts your rent and any expenses you have entered. The remaining savings buffer shows whether the property is genuinely affordable day-to-day, not just on paper.

References & External Sources

Authoritative data and guidance cited throughout this article:

- Office for National Statistics (ONS) — Private Rent and House Prices, UK: May 2026

- Data on average UK monthly rents by region and local authority, including the April 2026 national average of £1,381/month.

- https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/privaterentandhousepricesuk/may2026

- UK Government — Tenant Fees Act 2019

- Legislation capping tenancy deposits at five weeks’ rent and restricting what landlords can charge.

- https://www.legislation.gov.uk/ukpga/2019/4/contents

- MoneyHelper (MaPS) — How Much Rent Can You Afford?

- Government-backed guidance on setting a rent budget and understanding affordability checks.

- https://www.moneyhelper.org.uk/en/homes/renting/how-much-rent-can-you-afford

- HM Revenue & Customs — Income Tax Rates and Allowances 2025–26

- Personal allowance and tax band figures are used to estimate net take-home pay in this calculator.

- https://www.gov.uk/income-tax-rates

- Shelter England — Private Renting: Affordability and Referencing

- Charity guidance on tenant referencing requirements, guarantors, and what to do if you fail a check.

- https://england.shelter.org.uk/housing_advice/private_renting

Disclaimer: This calculator provides estimates for informational and budgeting purposes only. Results are based on the 30× annual income rule and standard UK letting agent benchmarks as used by referencing providers including Homelet, Let Alliance, and OpenRent as of 2025–2026. Actual referencing decisions depend on individual lender or agent criteria, credit history, and employment verification. This tool does not constitute financial or legal advice. Always confirm affordability thresholds directly with the letting agent or referencing provider before making a tenancy application.

Last Update: June 2026