Table of Contents

ToggleDebt Snowball Calculator — Find Your Debt-Free Date Fast

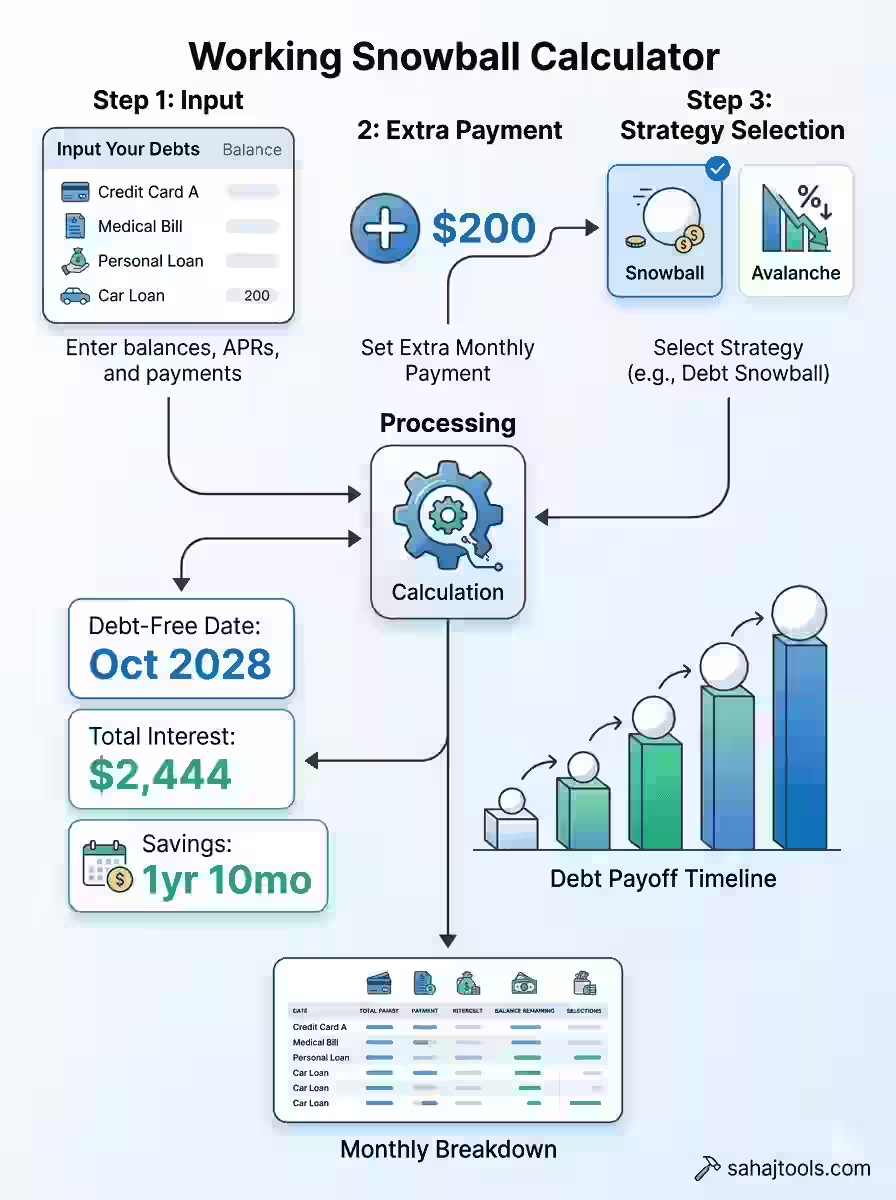

This debt snowball method calculator shows your exact debt-free date by targeting the smallest balance first, then rolling each freed-up payment into the next debt. Enter your balances, APRs, and minimums, add an extra monthly amount, and this debt-free date calculator snowball builds your complete payoff plan and amortization schedule in seconds.You have four debts. A credit card that never seems to shrink. A medical bill from last year. A car loan. A personal loan. Every month you make minimum payments and still feel like you’re going nowhere. Sound familiar?

SnowballCalc

Snowball Debt Calculator

See your debt-free date, compare strategies, and build your ultimate payoff plan — in seconds.

❄ Snowball Method🏔 Avalanche Comparison📊 Full Amortization

1 Enter Your Debts

Add every debt — credit cards, loans, medical bills, student debt. Up to 15 debts supported.

#Debt / Creditor NameBalance ($)APR (%)Min. Payment ($)

No debts yet. Click Add Debt to get started.

2 Extra Monthly Payment

Any amount above your minimum payments you can afford each month.

$

3 Payoff Strategy

Choose how to prioritize which debt to attack first.

Snowball builds motivation through quick wins. Avalanche saves the most money mathematically.

Your Payoff Plan

🎯

Debt-Free Date

—

—

💳

Total Interest Paid

—

with this strategy

💚

Interest Saved

—

vs. minimum payments only

⏱

Time Saved

—

vs. minimum payments only

Strategy Comparison

Snowball vs. Avalanche vs. Minimum Payments Only

Debt Payoff Timeline

When each debt will be eliminated — in order of attack

Monthly Breakdown

Complete month-by-month amortization schedule

| # | Date | Total Payment | Interest | Principal | Balance Remaining | Milestone |

|---|

related finance & business calculators

What Is a Debt Snowball Calculator?

A debt repayment calculator snowball is a financial planning tool that maps every debt you owe — credit cards, medical bills, personal loans, car loans — into a single, prioritized payoff sequence. It is the digital version of the strategy Dave Ramsey made mainstream: the Ramsey debt snowball tool concept, which has helped millions of Americans eliminate debt by focusing on quick psychological wins rather than mathematical optimization.

The core mechanic is simple. The calculator ranks your debts by balance and directs all available extra money at the smallest one first. The moment that balance hits zero, its monthly payment rolls forward — like a debt snowball momentum builder — adding weight and speed to the attack on the next balance. Repeat that cycle across every account and your monthly strike power grows with each debt you clear.

As a multiple debts payoff planner, this tool handles up to 15 simultaneous balances, making it useful whether you have two credit cards or a full mix of revolving and installment debt. It also addresses the single biggest reason people fail at debt repayment: motivation. The debt snowball psychological motivation behind the method — eliminating accounts quickly and visibly — keeps more people on track than the mathematically superior avalanche strategy does in practice.

A credit card debt snowball calculator works on the same engine: enter your card balances smallest to largest, set an extra payment, and watch the tool plot your exact escape date.

How the Debt Snowball Method Is Calculated

The calculator runs a multi-debt amortization loop using a precise payoff order smallest to largest balance. Here is the full sequence:

- Sort all debts by current balance, ascending.

- Calculate monthly interest on each account: Balance × (APR ÷ 12).

- Apply the required minimum to every debt except the top-priority account.

- Send all remaining funds — minimums freed up plus extra contribution — to the smallest balance.

- When that balance reaches $0, redirect its minimum payment to the next account in line.

- Continue until the final balance is cleared.

The underlying debt snowball mathematical formula is the standard amortization equation:

M = P × [r(1 + r)ⁿ] ÷ [(1 + r)ⁿ − 1]

Where M = monthly payment, P = remaining principal, r = monthly interest rate (APR ÷ 12), and n = number of remaining payment periods. Excel and Google Sheets users will recognise this as the NPER formula debt payoff equivalent — NPER returns the number of periods needed to retire a balance at a given rate and payment, which is exactly what this calculator solves iteratively across multiple accounts.

The debt snowball monthly payment calculator feeds this formula fresh inputs every month: updated balances, accrued interest, and the rolling payment pool. The output for each month includes total payment, interest charged, principal reduced, and balance remaining — producing a full debt snowball amortization schedule from today through your final zero-balance month. Total interest paid snowball method results are summed across all accounts and displayed alongside the interest-only and minimum-payment-only benchmarks so you can see exactly what the strategy saves you.

Step-by-Step: How to Use This Calculator

The interface has three input stages and one results panel. Work through them in order:

Step 1 — Enter Every Debt: Click + Add Debt for each balance you owe. For each entry, fill in the creditor name, current balance, APR, and minimum monthly payment. The tool accepts credit cards, personal loans, medical bills, car loans, and student debt — any account with a fixed or variable minimum.

Step 2 — Set Your Extra Monthly Contribution: This is where the extra payment debt snowball calculator gets its power. In the Extra Monthly Payment field, enter the amount above your combined minimums that you can consistently commit each month. This figure drives your debt snowball extra money allocation — every dollar here directly accelerates the payoff order and shrinks total interest paid.

Step 3 — Choose Your Strategy: Select Snowball (smallest balance first) or Avalanche (highest APR first). The results panel shows both side-by-side so you can evaluate the trade-off instantly.

Step 4 — Calculate and Read Your Plan: Click Calculate My Payoff Plan. The results panel displays four headline numbers: your debt freedom date calculator snowball output (your exact month and year of becoming debt-free), total interest paid, interest saved versus minimum payments only, and total time saved. Below that, the debt snowball payoff timeline shows a visual bar for each debt, indicating when it gets eliminated in the attack sequence. The monthly breakdown table is your built-in minimum payment rollover calculator — it shows exactly when each account hits zero and how its payment rolls into the next target, month by month.

Step 5 — Export or Copy: Download the full schedule as an XLSX file or copy a summary to share. Click Reset All to model a new scenario.

Worked Example: Four Debts, 24 Months to Zero

# | Debt | Balance | APR | Min. Payment |

1 | Medical Bill | $850 | 0% | $50 |

2 | Credit Card A | $2,500 | 19.99% | $75 |

3 | Personal Loan | $6,200 | 12.5% | $160 |

4 | Car Loan | $11,400 | 7.9% | $290 |

Combined minimums: $575/month. Extra contribution: $360. Total monthly payment: $935.

Payoff sequence and results:

- Medical Bill — cleared Sep 2026 (month 3)

- Credit Card A — cleared Feb 2027 (month 8)

- Personal Loan — cleared Oct 2027 (month 16) — personal loan snowball payoff accelerated by the rolled-over $625 monthly strike from the two cleared accounts

- Car Loan — cleared Jun 2028 (month 24)

Debt-Free Date: June 2028 — 2 years from today

Total interest paid snowball method: $2,170

Interest saved vs. minimum payments only: $2,626

Time saved vs. minimum payments only: 2 years 2 months

The small wins debt repayment motivation built into this sequence is visible in the numbers: the medical bill disappears in just three months, Credit Card A in eight. Those early eliminations add $125/month to the pool attacking the personal loan, then $285/month to the final car loan balance — that is the debt snowball payoff speed versus avalanche advantage in human terms. The avalanche saves $81 more in interest over the same period but produces no eliminated account until month 8.

Snowball vs. Avalanche: Full Strategy Comparison

Understanding how does debt snowball work versus the avalanche method is the most common question new users bring to this calculator. The debt payoff comparison snowball vs avalanche comes down to one trade-off: psychology versus mathematics.

Strategy | Payoff Time | Total Interest | Debt-Free Date |

Debt Snowball | 2 yrs | $2,170 | Jun 2028 |

Debt Avalanche | 2 yrs | $2,089 | Jun 2028 |

Minimum Payments Only | 4 yrs 2 mos | $4,795 | Aug 2030 |

The debt avalanche method calculator targets the highest APR balance first, always minimizing total interest paid. In our example it saves $81 over snowball — a real but modest difference. Run a debt avalanche method calculator alongside this tool to see the gap for your specific balances; when your smallest debt also carries a high APR, the two strategies converge and the difference shrinks close to zero.

The debt snowball psychological benefits are well-documented in behavioral finance research. Eliminating an account entirely — regardless of its size — produces a measurable motivation boost that makes plan abandonment significantly less likely. The credit card payoff snowball method is especially effective here because card balances tend to be smaller than installment loans, meaning the first win comes fast.

One key debt snowball interest rate ignore principle: the method deliberately does not use APR to set payoff order. Interest still accrues on every balance every month — the calculator accounts for that in every row of the amortization schedule — but the sequencing decision ignores rate entirely. That is by design, not an oversight.

The debt snowball minimum payment redirect is the mechanical heart of the method. When account #1 clears, its minimum does not get absorbed back into discretionary spending — it immediately joins the payment attacking account #2. Missing this step is the most common reason real-world snowballs stall.

Factors That Affect Your Debt Snowball Results

Your debt snowball extra money allocation is the single most powerful variable in the model. Doubling your extra payment from $180 to $360 in our example cut the payoff timeline by over a year. Even an additional $50/month makes a measurable difference on short-balance accounts at the top of the stack.

Following your debt snowball method steps consistently matters as much as the initial calculation. The model assumes fixed monthly payments, no new debt, and that every minimum redirect happens on schedule. Drift in any of these assumptions — a missed redirect, a new charge on a cleared card — resets the momentum the calculator built in.

Other variables that shift your results: number of accounts (more accounts mean more rollover events, each of which accelerates the snowball), balance distribution (several small balances produce early wins faster than one large small balance), and APR on each target (a high-rate small balance cleared early incidentally saves more interest than the calculator’s baseline projects).

Common Mistakes to Avoid

Not redirecting minimums immediately. The debt snowball minimum payment redirect must happen the same month a balance clears. Spending that freed-up minimum elsewhere breaks the compounding effect entirely.

Using a generic spreadsheet instead of a dedicated tool. A best debt snowball spreadsheet template like those on Vertex42 debt snowball spreadsheet pages works for simple scenarios, but it requires manual updates each month and does not recalculate dynamically when you change an input. A live calculator handles the rolling amortization automatically and flags your exact payoff date without manual formula maintenance.

Entering the wrong APR. Use the APR from your most recent billing statement, not a promotional or introductory rate. Promotional 0% periods affect strategy — a balance expiring out of a 0% window should often be prioritized above strict snowball order.

Adding new debt mid-plan. The calculator models a closed system. New charges to any account restart that balance’s elimination timeline and delay every subsequent rollover.

Treating the extra payment as variable. The snowball’s projected timeline assumes your extra contribution is consistent every month. Build the plan around your minimum sustainable amount; treat windfalls as bonuses that accelerate the schedule, not as the baseline.

related finance & banking calculators

- Money Market Calculator: Plan your investments alongside spousal support payments. This tool helps you estimate returns on savings or investments, ensuring you can meet financial obligations while growing your wealth.

Frequently Asked Questions

The debt snowball method ranks your debts from smallest to largest balance and directs every available extra dollar at the smallest account first while paying minimums on all others. When the smallest balance clears, its payment rolls into the next account in line. The process repeats — with a growing monthly payment pool — until every balance is zero. The method prioritizes motivation through quick early wins over mathematical interest minimization.

The debt avalanche saves more total interest because it targets high-APR balances first. The debt snowball produces faster early wins, which behavioral research shows improves completion rates. For anyone who has previously abandoned a debt plan, the snowball's psychological structure often delivers better real-world results despite the small additional interest cost. Run both through a debt avalanche method calculator to compare the exact dollar difference for your balances.

Four inputs per debt: current outstanding balance, APR, minimum required monthly payment, and account name. One household-level input: the extra monthly amount above your combined minimums you can consistently contribute. That is everything the calculator needs to generate your full schedule.

Yes — intentionally. The debt snowball interest rate ignore principle means APR does not determine payoff order; only balance size does. Interest still accrues on every account every month and is reflected in the amortization schedule, but it plays no role in which debt gets attacked first. This is the fundamental difference between snowball and avalanche.

Any consistent amount accelerates the plan, but the impact scales non-linearly. In our worked example, $360/month of extra contribution cut the timeline from 4+ years to 2 years. Start with what your budget reliably supports. Use a budget calculator to identify your realistic debt snowball extra money allocation before committing to a number, then treat any irregular income as a bonus accelerator.

Its minimum payment immediately redirects to the next smallest balance — this is the debt snowball minimum payment redirect that gives the method its compounding momentum. The total amount you send to creditors each month stays the same; it simply concentrates on one fewer account. Never absorb a cleared minimum back into discretionary spending.

Payoff time depends on total debt, APR mix, and extra monthly contribution. In our four-debt, $20,196 example with $360 extra per month, full payoff took 24 months versus 50 months on minimums only. The calculator generates a precise month-by-month timeline for your specific inputs. Every $100 of additional monthly contribution typically removes 6–9 months from a $15,000 debt load at average credit card rates.

The interest difference depends on your specific balance and APR mix. In our example, snowball paid $2,170 in total interest versus $2,089 for avalanche — an $81 difference over two years. When your smallest balances also carry high APRs, the two strategies converge and the gap shrinks to near zero. Both strategies save dramatically compared to minimum payments only, which would cost $4,795 in interest over 50 months in the same scenario.

The debt snowball psychological benefits come from account elimination. Paying down a balance feels abstract; closing an account entirely feels like a concrete win. Behavioral economics research consistently shows that completing discrete goals — even small ones — produces a motivation boost that reinforces the behavior. The method is structured specifically to deliver that win as early as possible, often within the first 1–3 months.

Yes. The credit card payoff snowball method works identically to the full multi-debt version — sort cards smallest balance to largest, attack the smallest while paying minimums on the rest, redirect each cleared card's minimum to the next. It is equally valid applied only to cards, only to installment loans, or to any mixed set of balances.

Disclaimer

This calculator provides estimates for educational and planning purposes only. Results are based on the balances, APRs, and payment amounts entered and assume fixed interest rates, no new charges, and consistent monthly payments throughout the payoff period. Actual payoff timelines and interest costs will vary based on your lender’s compounding method, minimum payment changes, fees, and changes in your financial situation. This tool does not constitute financial advice. Consult a licensed financial counselor or certified credit counselor before making significant debt repayment decisions.

References & Authoritative Sources

The following authoritative sources underpin the data, formulas, and guidance presented in this article. Each is cited inline in the relevant sections above.

- Consumer Financial Protection Bureau (CFPB) — Debt Repayment Tools & Guidance

- Federal Reserve — Consumer Credit Statistical Release (G.19): Credit Card Interest Rates

- Investopedia — Debt Snowball Method: Definition, How It Works, and Pros & Cons

- NerdWallet — Debt Snowball vs. Debt Avalanche: Which Strategy Is Right for You?

- Harvard Business Review — “To Pay Off Loans, Pay Attention to the Smallest Ones First” (Behavioral Research)

Last Update: June 2026