Table of Contents

ToggleTax Equivalent Yield Calculator: Find Your Real Bond Return

Tax-equivalent yield is the yield a taxable bond would need to pay to match the after-tax return of a tax-free municipal bond. The Tax Equivalent Yield Calculator converts a tax-free yield into its taxable equivalent using your marginal tax rate, so you can directly compare municipal bonds against taxable bonds, CDs, or money market funds on an apples-to-apples basis.

Financial Tool

Taxable Equivalent

Yield Calculator

Compare tax-free bonds against taxable investments — instantly and accurately.

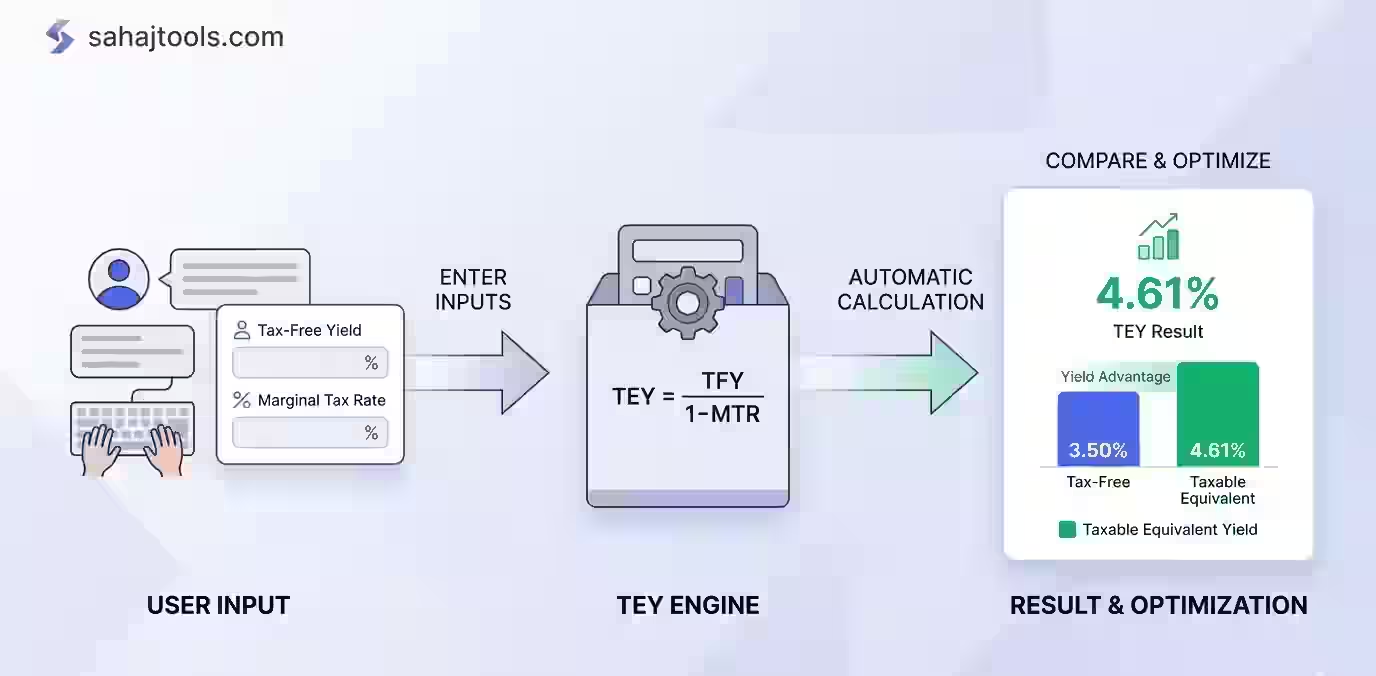

FormulaTEY = Tax‑Free Yield ÷ (1 − Marginal Tax Rate)

Result

Your Taxable Equivalent Yield

—%

Taxable Equivalent Yield

Tax-Free YieldTaxable Equivalent

For informational purposes only. Not financial advice. Consult a qualified tax professional for personalized guidance.

Reset Calculator?

This will clear all inputs and results. Saved session data will also be removed.

related finance calculators

What Is a Tax Equivalent Yield Calculator?

A Tax Equivalent Yield Calculator is a tool that translates the tax-free yield on a municipal bond into the taxable yield an equivalent taxable investment would need to offer to deliver the same after-tax income. Municipal bond interest is generally exempt from federal income tax, and in many cases from state income tax as well when the bond is issued within your own state of residence. Because of that tax-exempt status, a municipal bond’s stated yield isn’t directly comparable to the yield on a taxable bond, CD, or corporate note — a 3.5% tax-free yield can be worth considerably more than 3.5% to an investor in a high tax bracket.

This calculator removes the guesswork. Enter your tax-free yield and marginal tax rate, and it returns the taxable-equivalent yield — the exact return a taxable bond would need to match your municipal bond’s after-tax payout. It’s most useful for tax-conscious investors comparing muni bonds against taxable alternatives, financial advisors building fixed-income allocations, and retirees managing taxable investment income.

How Tax-Equivalent Yield Is Calculated

The tax-equivalent yield formula converts a tax-free yield into pre-tax terms using one straightforward ratio:

TEY = Tax-Free Yield ÷ (1 − Marginal Tax Rate)

Where:

- Tax-Free Yield is the yield quoted on the municipal bond (coupon rate or yield-to-maturity), entered as a decimal or percentage.

- Marginal Tax Rate is the tax rate applied to your last dollar of income — the rate at the top of your tax bracket, not your average (effective) tax rate.

- TEY (Taxable Equivalent Yield) is the pre-tax yield a taxable bond would need to produce the same after-tax income as the tax-free bond.

The logic behind the formula is simple: if you keep only (1 − tax rate) of every dollar a taxable bond pays you, then dividing the tax-free yield by that same fraction tells you how much pre-tax yield is required to net the identical after-tax amount. If you’re adding state or local tax, the calculator combines it with your federal rate into a single combined marginal tax rate before applying the same division — for example, a 24% federal rate plus a 5% state rate produces a 29% combined rate (assuming the state tax isn’t itself deductible against federal tax in your situation).

How to Use the Tax Equivalent Yield Calculator

- Enter your Tax-Free Yield. Type the yield quoted on your municipal bond (for example, 3.5) into the Tax-Free Yield field.

- Enter your Federal Marginal Tax Rate. Type your rate directly, or tap one of the Quick Pick buttons — 10%, 12%, 22%, 24%, 32%, 35%, or 37% — which correspond to the current IRS federal income tax brackets.

- Add State or Local Tax (optional). If your municipal bond income is also subject to state or local tax — which is common unless the bond was issued in your state of residence — tap “Add State / Local Tax” and enter that rate to get a combined-rate result.

- Tap Calculate TEY. The calculator instantly returns the taxable-equivalent yield: the pre-tax return a taxable bond would need to match your tax-free investment.

Worked Examples

Example 1 — Federal bracket only. An investor in the 24% federal marginal tax bracket is considering a municipal bond yielding 3.5% tax-free.

TEY = 3.5% ÷ (1 − 0.24) = 3.5% ÷ 0.76 = 4.61%

A taxable bond, CD, or money market fund would need to yield 4.61% before tax to match this muni bond’s after-tax return. Any taxable alternative paying less than 4.61% leaves this investor worse off after taxes.

Example 2 — Combined federal and state tax. An investor in the 35% federal bracket also pays 5% state income tax on out-of-state municipal bond interest, for a 40% combined marginal rate. Their tax-free yield is 4.0%.

TEY = 4.0% ÷ (1 − 0.40) = 4.0% ÷ 0.60 = 6.67%

At a 40% combined marginal rate, this investor would need a taxable bond yielding 6.67% just to break even with the 4.0% tax-free muni — a gap that widens sharply as combined tax rates climb.

Tax-Equivalent Yield by Tax Bracket (3.5% Tax-Free Yield)

Federal Marginal Tax Rate | Tax-Free Yield | Taxable-Equivalent Yield |

10% | 3.5% | 3.89% |

12% | 3.5% | 3.98% |

22% | 3.5% | 4.49% |

24% | 3.5% | 4.61% |

32% | 3.5% | 5.15% |

35% | 3.5% | 5.38% |

37% | 3.5% | 5.56% |

This bond yield comparison shows why the same tax-free municipal bond yield becomes more valuable as your tax bracket rises — the muni vs. taxable bond gap widens steadily from the 10% bracket to the 37% bracket. Investors in the top brackets often find municipal bonds offer the highest after-tax return among comparable fixed-income options, even when their stated yield looks lower than a taxable bond’s.

Risk Factors and Important Considerations

- Net Investment Income Tax (NIIT): High earners — modified adjusted gross income above $200,000 (single) or $250,000 (married filing jointly) — owe an additional 3.8% NIIT on net investment income from taxable bonds, dividends, and capital gains. These thresholds are not adjusted for inflation. Municipal bond interest is excluded from NIIT, which makes the taxable-equivalent yield gap even larger for affected investors than the federal bracket alone suggests.

- Alternative Minimum Tax (AMT): Interest from certain “private activity” municipal bonds can be subject to AMT, which may reduce or eliminate the tax-free benefit for some high-income taxpayers. Always check a specific bond’s AMT status before assuming it’s fully tax-exempt.

- Credit risk: Municipal bonds historically default less often than many taxable alternatives, but they are not risk-free. Review the issuer’s credit rating before comparing yields.

- Interest rate and price risk: Tax-equivalent yield measures income only — it does not account for how bond prices move when interest rates change. A bond’s market value can fall even while its stated yield stays the same.

- In-state vs. out-of-state exemption: Many states only exempt municipal bond interest from bonds issued within that same state. Out-of-state muni interest is often still taxable at the state level, which is why the optional state/local tax field matters.

- Past performance does not guarantee future results. This calculator is not investment advice and does not account for your full financial picture, liquidity needs, or risk tolerance.

Common Mistakes to Avoid

- Using your effective tax rate instead of your marginal tax rate. Tax-equivalent yield is based on the rate on your last dollar of income, not your average tax rate — using the wrong one significantly understates the result.

- Forgetting state tax when comparing out-of-state municipal bonds. Skipping the state/local add-on overstates a muni bond’s after-tax advantage if the interest is actually taxable in your state.

- Ignoring NIIT for high-income investors. Leaving out the 3.8% NIIT on taxable alternatives understates how much more attractive municipal bonds become for investors above the MAGI thresholds.

- Treating tax-equivalent yield as a total-return measure. The calculation reflects income yield only — it ignores price risk, call risk, and credit risk, which still need separate evaluation.

- Applying last year’s tax bracket. Federal tax bracket thresholds are adjusted for inflation annually; recalculate with the current year’s bracket and rate.

related finance & banking calculators

- Money Market Calculator: Plan your investments alongside spousal support payments. This tool helps you estimate returns on savings or investments, ensuring you can meet financial obligations while growing your wealth.

Frequently Asked Questions

Tax-equivalent yield is the pre-tax yield a taxable investment would need to earn to match the after-tax income of a tax-free municipal bond. It allows direct comparison between tax-exempt and taxable bonds.

Divide the municipal bond's tax-free yield by one minus your marginal tax rate. The result tells you what a taxable bond would need to yield, before tax, to match your tax-free bond's after-tax return.

The formula is TEY = Tax-Free Yield ÷ (1 − Marginal Tax Rate). If you're including state tax, combine your federal and state marginal rates first, then apply the same formula.

Municipal bonds pay tax-exempt interest, usually at a lower stated yield than taxable bonds. Once converted to a taxable-equivalent yield, however, municipal bonds frequently outperform comparable taxable bonds for investors in higher tax brackets, even though their headline yield looks smaller.

Use your marginal tax rate — the rate that applies to your last dollar of taxable income — not your effective (average) tax rate. If the municipal bond's interest is also taxable in your state, add your state marginal rate using the calculator's optional state/local tax field.

Federal and state marginal rates combine into your total marginal tax rate, which directly increases the calculated TEY. The 3.8% Net Investment Income Tax applies only to taxable investment income above MAGI thresholds of $200,000 (single) or $250,000 (married filing jointly) — since municipal bond interest is excluded from NIIT, high earners above these thresholds see an even larger after-tax advantage from munis than the federal bracket alone shows.

It depends on whether the taxable bond's actual yield is above or below your calculated tax-equivalent yield. If the taxable bond pays more than your TEY result, it wins on an after-tax basis; if it pays less, the municipal bond delivers a higher after-tax return.

The break-even yield is exactly the taxable-equivalent yield this calculator returns. At that exact yield, the taxable bond and the tax-free municipal bond produce identical after-tax income — any taxable yield above that figure wins, and any yield below it loses to the municipal bond.

Tax-free yield converts to pre-tax (taxable-equivalent) yield by dividing it by one minus your marginal tax rate. To compare several bonds at once, run each one's tax-free yield through the calculator using the same marginal tax rate, then rank the resulting taxable-equivalent yields alongside the actual yields of any taxable bonds you're considering — the highest after-tax result wins.

Source & Accuracy Note

Federal marginal tax rates used in this calculator’s quick-pick options (10%, 12%, 22%, 24%, 32%, 35%, 37%) reflect the seven federal income tax brackets for the 2026 tax year, made permanent under the One Big Beautiful Bill Act (OBBBA) and published by the Internal Revenue Service. The 3.8% Net Investment Income Tax referenced in the Risk Factors section is also set by the IRS and applies at the MAGI thresholds noted above. Tax brackets and thresholds are adjusted annually for inflation — always verify current-year rates directly with the IRS or your state Department of Revenue before making an investment decision based on this calculator’s output.

Disclaimer

This Tax Equivalent Yield Calculator is provided for informational and educational purposes only and does not constitute investment, tax, or financial advice. Bond markets carry risk, including the risk of loss of principal, and past performance does not guarantee future results. Tax treatment of municipal bond interest varies by state, bond type, and individual circumstances. Consult a licensed financial advisor and a qualified tax professional before making any investment decision based on this tool’s output.

Last Update: June 2026